Context

Sustainability reporting requirements are moving toward greater convergence as reflected in the application of the International Sustainability Standards Board (ISSB). In the interim challenges remain for Investment Firms trying to navigate overlapping disclosures and a complex regulatory landscape.

Large Investment Firms (with AUM above £50 billion) were required to publish their Sustainability Disclosure Requirements (SDR) entity disclosures by 2 December 2025. Alpha FMC took the opportunity to review a sample of these reports across a wide range of firm types.

Our analysis highlights emerging trends in how firms are approaching both the structure and content of their reports, and distils key takeaways to help teams strengthen their own SDR reporting. Strong narrative, cohesion across sustainability disclosures, and a clear focus on materiality emerged as critical elements of effective reporting.

Trends Observed

Structure and Approach

Disclosure Alignment

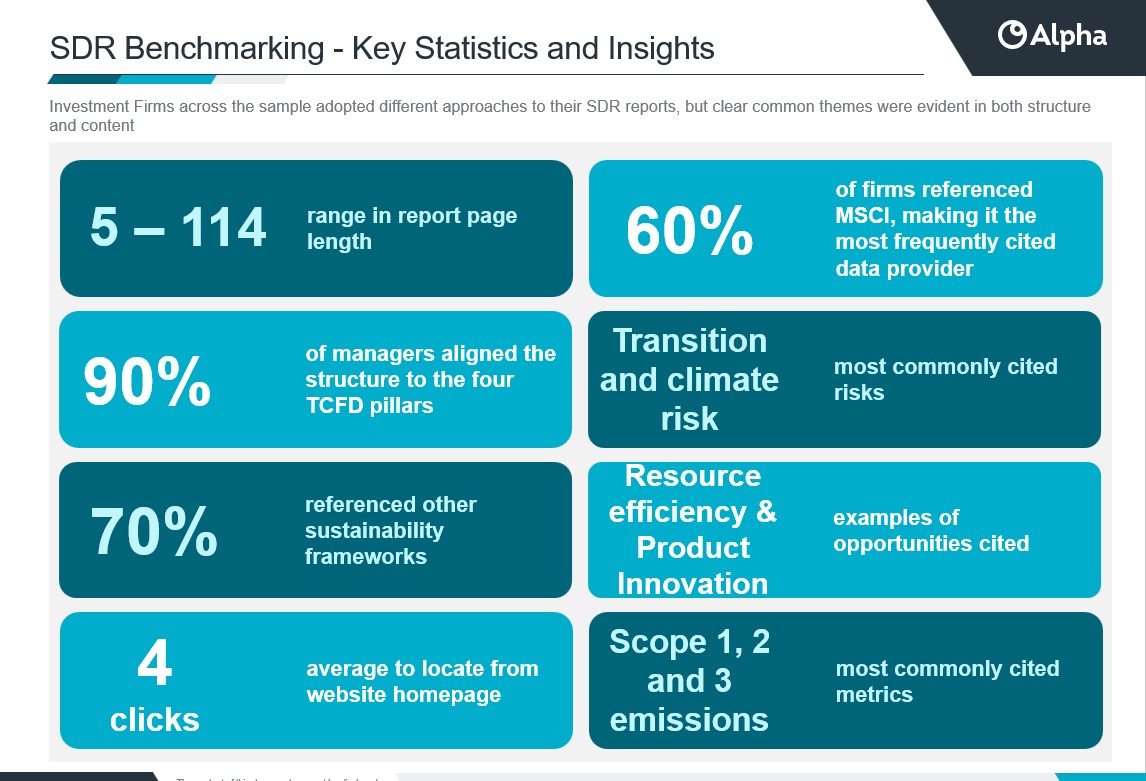

90% of Investment Firms aligned the structure of their reports to the Taskforce for Climate-Related Financial Disclosures (TCFD) framework and most stated that they should be read in conjunction with their TCFD report. A small number of firms (10%) went a step further and combined their SDR and TCFD disclosures. We also saw examples of alignment with the Taskforce for Nature-Related Financial Disclosures.

Where firms combined reporting, this stood out for articulating a clear sustainability and climate vision, framed around strategic priorities within the evolving sustainability policy landscape. This demonstrates the value of stepping back to define what sustainability means for the organisation and communicating it consistently, rather than fragmenting it across multiple reports.

Report Length

Length varied considerably ranging from 5 to 114 pages. Shorter reports often relied on cross-referencing other publications rather than providing substantive disclosure, which weakened the overall narrative. One firm presented disclosures in a tabular format mapping SDR requirements to existing reports, which was less effective as a standalone document. While there is no prescribed best-practice length, reports should be sufficiently comprehensive to provide clear and decision-useful disclosures.

Content

Methodology and Frameworks

Good practice entails identifying information that is most useful and relevant to consumers, which many firms achieved by leveraging established frameworks, proprietary frameworks and internal tools. 70% of Investment Firms explicitly referenced at least one of the following sustainability frameworks to inform their materiality assessments and the selection of reporting metrics: IFRS S1, SASB, GRI, SFDR, the GHG Protocol Corporate Accounting and Reporting Standard, and the ICARA framework*.

Risks and Opportunities Management

The majority of reports focused on governance and risk management frameworks rather than explicitly identifying their most material sustainability risks and opportunities and how these are being addressed, as would be considered best practice to meet reporting requirements.

Where specific risks were described, they were often implicit or located elsewhere in the report, such as in the strategy section or in linked publications, with few firms explicitly highlighting their sustainability opportunities. As a result, these risks and opportunities were often difficult for readers to locate within the reports. From a broader Consumer Duty perspective, not explicitly calling out risks/opportunities made reports harder to navigate and doesn’t align with expected good practice.

Metrics and Targets

Material metrics varied across firms with climate and emissions measures (Scopes 1, 2, and 3), being the most commonly reported. Other frequently disclosed metrics included activity-based stewardship, workforce, diversity and regulatory measures (e.g. the number of SDR labels or Sustainable Finance Disclosure Regulation Article 8 and 9 funds).

Selecting metrics that reflect material topics is leading practice as it helps readers to understand how these are being measured and addressed.

Data Providers

Best practice involves ensuring robust data and methodologies are clearly documented and support the tracking and monitoring of metrics tied to the specific sustainability risks identified by the firm. Firms widely cited their engagement with external providers such as MSCI and Sustainalytics alongside proprietary data platforms for this purpose.

Source: Alpha SDR Entity Reports - 2025 Benchmarking

Key Takeaways to Strengthen your SDR Entity Reporting

- Define a clear narrative and vision: Best-practice reports are well structured and supported by a strong narrative across all sustainability reporting that sets the strategic context i.e. where the firm is today, where it aims to be, and how its metrics and targets align with the wider business strategy to realise these ambitions.

- Focus on what is material to your business: Tailor reporting to what matters most to your business and audience. Cover key sustainability topics (such as climate, your workforce, and your underlying investments) and explain their impact on your strategy, operations, and financial planning. To be clear and informative, this should cover key risks and opportunities, the metrics and targets tracked, and performance against them.

- Streamline sustainability reporting: There may be opportunities to streamline disclosures by aligning with TCFD requirements or, where appropriate, combining reports. Teams should consider this in the next reporting cycle to make better use of existing information, reduce duplication, and deliver clearer, more cohesive reporting, particularly in light of the FCA’s consultation on aligning reporting requirements. Jurisdictions where ISSB is already mandated such as Australia provide a notable example with many Investment Firms positioning themselves as early leaders in streamlining sustainability reporting.

At Alpha FMC, we have substantial experience supporting clients in their sustainability reporting journey, so please get in touch if you would like to discuss this further with us.

Footnotes:

* IFRS S1 — International Financial Reporting Standards Sustainability Disclosure Standard S1

SASB — Sustainability Accounting Standards Board

GRI — Global Reporting Initiative

SFDR — Sustainable Finance Disclosure Regulation

GHG Protocol Corporate Accounting and Reporting Standard — Greenhouse Gas Protocol Corporate Accounting and Reporting Standard

ICARA framework — Internal Capital and Risk Assessment framework

About the Authors

Stephanie Taylor

Consultant, Sustainability & Responsible Investment Practice

Stephanie is a Consultant in Alpha's Sustainability & Responsible Investment practice. She advises on Sustainability Disclosure Requirements (SDR) initiatives and has been tracking labels and developments in this space. She led the benchmarking of SDR Entity reports, distilling key insights for managers preparing disclosures in 2026. Her broader experience spans Sustainability Operating Model design and wider business transformation initiatives.

Lisa Aspinall

Senior Manager, Sustainability & Responsible Investment Practice

Lisa is a Senior Manager within Alpha’s Sustainability & Responsible Investment practice with 12 years experience in sustainability and regulation. She leads the SDR proposition and has helped several asset managers to implement SDR across labelled and unlabeled funds and produce the required disclosures. She has also supported managers to design and implement their end to end sustainability operating models. Her background is in regulation having worked for the FCA and the French AMF.

Carole Boissat

Senior Manager, Sustainability & Responsible Investment Practice

Carole is a Senior Manager within Alpha’s Sustainability & Responsible Investment practice with 10+ years' experience in Sustainability, regulatory, risk management and big data. She has worked on a variety of Sustainability-related projects within Asset Management, from regulations to operational risk and Target Operating Model design. More recently, Carole has also performed various peer benchmarking analyses on Sustainability topics such as TCFD, SDR and Transition Planning.